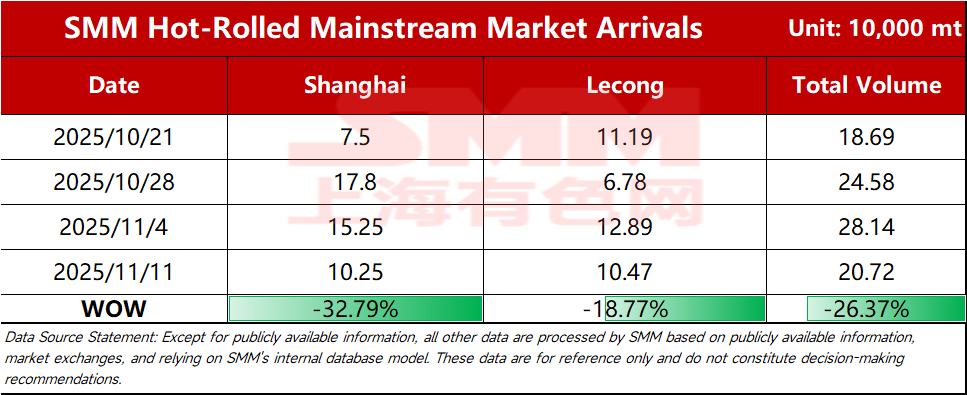

SMM Steel, November 11 – According to SMM statistics, estimated total resource shipments in major markets this week were 107,200 mt, down 26.37% WoW from last week's shipping level. By market:

Table 1: Comparison of Arrivals in Major Markets

Data source: SMM Steel

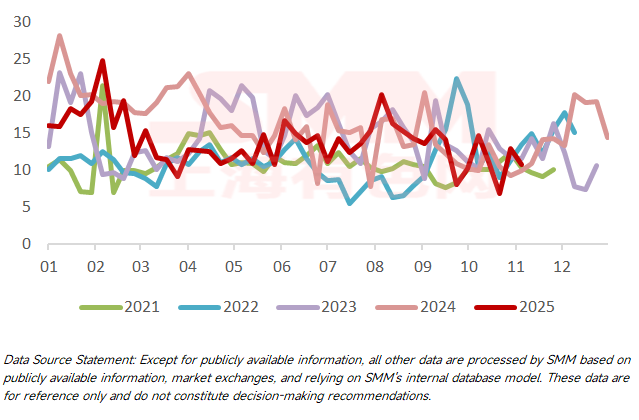

Shanghai Market: Shipments to the Shanghai market continued to decrease this week. Specifically, shipments from steel mills in Northeast, North, and South China all declined, while shipments from East China mills remained stable. Looking ahead, recent hot-rolled coil prices have been in the doldrums, with no significant advantage in the price spread between East and South China. Additionally, transactions in the Shanghai market were average, coupled with inventory slightly higher than the same period in previous years, leading to weak ordering enthusiasm among merchants. Arrivals in the Shanghai market are expected to see no significant increase in the short term.

Chart 1: Arrivals in the Shanghai Market

Data source: SMM Steel

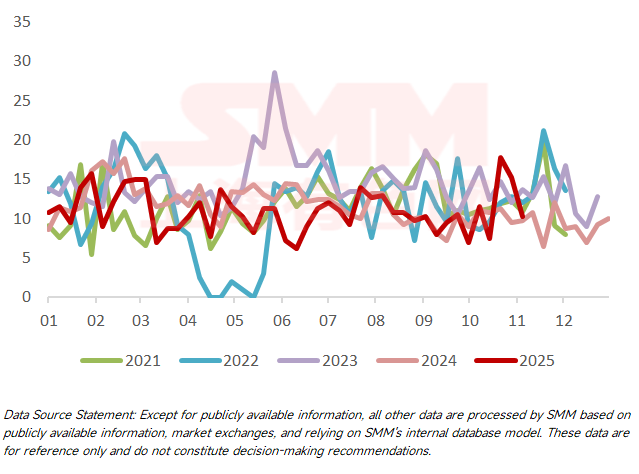

Lecong Market: Shipments to the Lecong market decreased WoW this week. Specifically, arrivals of resources from North China decreased WoW, while mainstream resources were largely stable WoW, with some steel mills still showing a preference for shipping to East China. Looking ahead, inventory in South China remains relatively high, and some steel mills still maintain certain shipping preferences. Meanwhile, WG plans to produce grade steel in the middle of the month. Arrivals are expected to remain at low levels in the short term.

Chart 2: Arrivals in the Lecong Market

Data source: SMM Steel

SMM releases hot-rolled shipment data for mainstream market flows every Tuesday. To subscribe or follow more other data, please scan the QR code below.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)